Factors Influencing Customer Intention to Use Cardless ATM Services: A Study of Government Savings Bank Customers

Article Sidebar

Main Article Content

Abstract

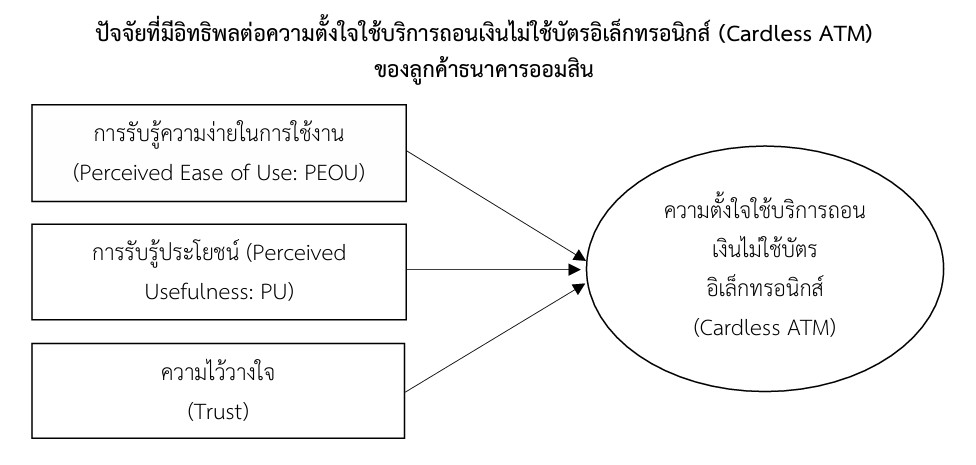

This study aimed to examine the factors influencing customers’ intention to use cardless ATM services of the Government Savings Bank (GSB) in the Bangkok Metropolitan Area. Specifically, the study investigated the relationships between perceived usefulness (PU), perceived ease of use (PEOU), trust, and behavioral intention to use cardless ATM services, based on the Technology Acceptance Model (TAM) integrated with the trust construct. A quantitative research design employing a survey method was adopted. The research instrument used for data collection was an online questionnaire, and the data were collected from Government Savings Bank customers in the Bangkok Metropolitan Area through an online system. Data were collected through an online questionnaire from 385 GSB customers who had prior experience using cardless ATM services. The sample size was determined using Cochran’s formula at a 95% confidence level. The collected data were analyzed using descriptive statistics and multiple regression analysis. The findings revealed that perceived usefulness, perceived ease of use, and trust had significant positive effects on customers’ intention to use cardless ATM services. The model explained 43.2% of the variance in customers’ intention to use the service (R² = 0.432). Among the three factors, perceived ease of use exerted the strongest influence, followed by perceived usefulness and trust. The results suggest that in the context of a state-owned bank serving diverse customer segments, including elderly and low-income groups, simplicity of system design plays a foundational role in technology adoption. The study contributes to the literature by extending TAM within the context of a public financial institution and provides practical implications for enhancing digital financial service adoption through user-friendly design, clear value communication, and strengthened institutional trust.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

ธนาคารแห่งประเทศไทย. (2566). Payment Systems Report 2023 (รายงานระบบการชำระเงิน ประจำปี 2566). กรุงเทพฯ: ธนาคารแห่งประเทศไทย.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319-340.

Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model. MIS Quarterly, 27(1), 51-90.

Kim, D. J., Ferrin, D. L., & Rao, H. R. (2008). A trust-based consumer decision-making model in electronic commerce. Decision Support Systems, 44(2), 544-564.

Kim, Y., Chan, H. C., & Gupta, S. (2007). Value-based adoption of mobile internet: An empirical investigation. Decision Support Systems, 43(1), 111-126.

Lichtenstein, S., & Williamson, K. (2006). Understanding consumer adoption of internet banking: An interpretive study in the Australian banking context. Journal of Electronic Commerce Research, 7(2), 50–66.

Nambiar, B. K., & Bolar, K. (2023). Factors influencing customer preference of cardless technology over the card for cash withdrawals: An extended technology acceptance model. Journal of Financial Services Marketing, 28(1), 58–73.

Pavlou, P. A. (2003). Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model. International Journal of Electronic Commerce, 7(3), 101–134.

Phothikitti, K. (2020). Factors influencing intentions to use cardless automatic teller machine (ATM). International Journal of Economics and Business Administration, 8(3), 40–56.

Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186–204.