Factors Influencing Consumers’ Intention to Use Informal Credit in Bangkok

Article Sidebar

Main Article Content

Abstract

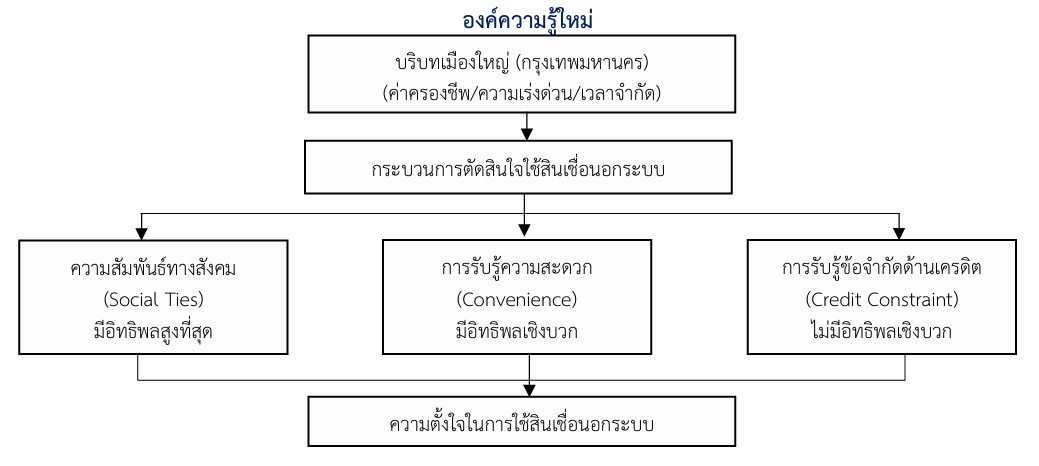

This study aimed to examine the influence of social ties, perceived convenience, and perceived credit constraints on consumers’ intentions to use informal credit in Bangkok. A quantitative research approach was employed, conceptualizing intention as a predictor of informal credit usage behavior. Data were collected from 385 respondents aged 20–60 years using a multi-stage sampling technique. A structured questionnaire was used as the data collection instrument, and the data were analyzed using descriptive statistics and multiple regression analysis. The results indicated that respondents reported high levels of agreement with all three factors. Social ties had the highest mean score, followed by perceived credit constraints and perceived convenience. The regression model explained 5.0% of the variance in the intention to use informal credit (R² = 0.050). Inferential analysis revealed that social ties had a statistically significant positive effect on the intention to use informal credit, and perceived convenience also had a statistically significant positive effect. In contrast, perceived credit constraints did not have a statistically significant effect. These empirical findings suggest that social networks and ease of access to funds are more influential in shaping consumers’ intentions to use informal credit than perceived constraints from formal financial institutions. The results have important implications for designing appropriate and sustainable policies to improve access to formal financial services.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

ธนาคารแห่งประเทศไทย. (2567). รายงานสถานการณ์หนี้ครัวเรือนไทยและเสถียรภาพระบบการเงิน. กรุงเทพฯ: ธนาคารแห่งประเทศไทย.

ปราณชนิน สังข์แสงใส. (2565). ปัจจัยที่ส่งผลต่อความตั้งใจใช้บริการสินเชื่อเพื่อคุณของธนาคารออมสินในจังหวัดปทุมธานี. (บริหารธุรกิจมหาบัณฑิต, มหาวิทยาลัยศรีนครินทรวิโรฒ).

เพชรรัตน์ สุทธิเทพ, สุธาสินี โพธิ์ชาธาร และ สมศักดิ์ จินตวัฒนกุล. (2567). ปัจจัยเชิงสาเหตุที่ส่งผลต่อความตั้งใจทำธุรกรรมการเงิน ผ่านโมบายแบงค์กิ้งของประชาชนในประเทศไทย. วารสารปัญญาภิวัฒน์, 16(1), 62–80.

มงคล วิมลรัตน์, ชัยธนัตถ์กร ภวิศพิริยะกฤติ และ พิมพ์พลอย ธีรสถิตย์ธรรม. (2568). อิทธิพลของปัจจัยด้านการรับรู้ของผู้ใช้ที่ส่งผลต่อความตั้งใจในการใช้งานนวัตกรรมศูนย์ดิจิทัลเพื่อการท่องเที่ยวและบริการของประเทศไทย. วารสารดุษฎีบัณฑิตทางสังคมศาสตร์, 15(1), 290–308.

แววมยุรา คำสุข, พัชรา โพชะนิกร, เอกชัย ไชยดา, ธีวินท์ นฤนาท และ อนัญญา บรรยงพิศุทธิ์. (2565). ปัจจัยที่มีอิทธิพลต่อความตั้งใจในการมีส่วนร่วมใช้บริการธุรกิจขนส่งพัสดุของกลุ่มผู้ค้าอีคอมเมิร์ซในประเทศไทย. วารสารวิจัยและพัฒนา มหาวิทยาลัยราชภัฏเลย, 17(60), 9–16.

ศูนย์วิจัยกสิกรไทย. (2567). แนวโน้มพฤติกรรมการใช้จ่ายและภาระค่าครองชีพของครัวเรือนไทยในเขตเมือง. กรุงเทพฯ: ธนาคารกสิกรไทย.

สำนักงานเศรษฐกิจการคลัง. (2567). รายงานภาวะเศรษฐกิจการคลังและสถานการณ์หนี้ครัวเรือนของประเทศไทย. กรุงเทพฯ: กระทรวงการคลัง.

สิริภักตร์ ศิริโท. (2566). การยอมรับเทคโนโลยีและความตั้งใจจะใช้เทคโนโลยีรถยนต์ไฟฟ้าของผู้บริโภคในเขตกรุงเทพมหานคร. วารสารบริหารธุรกิจเทคโนโลยีมหานคร, 20(2), 185–200.

Cochran, W. G. (1997). Sampling Techniques. (3rd ed.). New York: John Wiley & Sons.

Giddens, A. (2018). Sociology. (8th ed.). Cambridge: Polity Press.

Goldstein, E. B. (2014). Sensation and perception. (8th ed.). Stamford, CT: Cengage Learning.

Granovetter, M. S. (1973). The strength of weak ties. American Journal of Sociology, 78(6), 1360-1380.